ARIMA

Category: Rollforward & time series

Overview

Description | Forecasting function based on the autoregressive integrated moving average (ARIMA) model. Use when you want to forecast a time series from historical patterns without defining explicit driver nodes. |

|---|---|

Syntax |

|

Parameters |

|

Examples

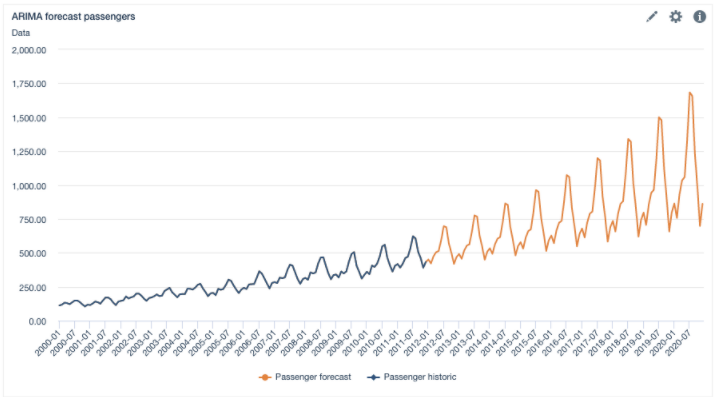

Monthly forecast from historical data

This example shows monthly historical passenger data used as the basis for an ARIMA forecast. The result keeps the historical observations and extends the series with forecasted periods to the end of the horizon.

Input node: Passenger historic

Data set: Passenger historic.xlsx )

Data horizon: 2000 - 2011

Year | Month | Value |

|---|---|---|

2000 | 2000-01 | 112 |

... | ... | ... |

2011 | 2011-12 | 432 |

Formula: ARIMA('Passenger historic', 1, 1, 1, 1, 0, 1, 12)

ARIMA horizon: 2000 - 2020

Year | Month | → ARIMA Result |

|---|---|---|

2000 | 2000-01 | 112 |

... | ... | ... |

2011 | 2011-12 | 432 |

2012 | 2012-01 | 450 |

... | ... | ... |

2020 | 2020-12 | 861 |

Chart:

Related Functions

Function | When to use instead |

|---|---|

When you want to project values with explicit driver nodes instead of forecasting from historical patterns alone. | |

When you want to smooth historical values over a rolling window instead of creating a forecast. |