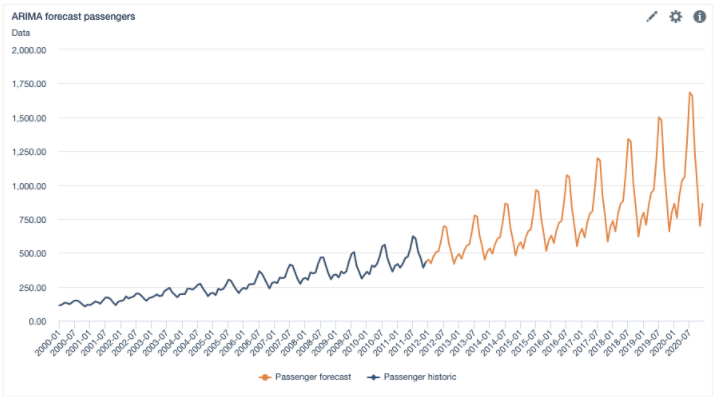

Forecasting function based on the autoregressive integrated moving average (ARIMA) model. More

Signature

ARIMA('Node', p, d, q, P, D, Q, m)

Parameters

Node: Node that contains the base data we want to base the forecasting on. It must contain at least one time level. Predictions is based on the time values in the node and it extends to the end of the horizon period. If the input data has a missing value in the time dimension the calculation fails. A time value is considered missing if the data has actual value(s) before and after the missing value. For example [2019, 2021] has missing value 2020, but [2020, 2021] or [2019, 2020] have no missing values.

p: the order (number of time lags) of the autoregressive model

d: the degree of differencing

q: the order of the moving-average model

P: autoregressive term for the seasonal part

D: differencing term for the seasonal part

Q: moving average term for the seasonal part

m: the number of periods in each season

Available from

3.6.0

The arguments p, d, q, P, D, Q, m can be nodes instead of single numbers, allowing to use different ARIMA arguments for individual time series in 'node'. Available since 3.7.0